IDC Opinion

The human vision system, which gathers and interprets information through sight, remains a critical aspect as part of one’s life as both a consumer and an employee (i.e., working as part of a private business or government entity). Vision is critical to performing routine tasks like navigating roadways and sidewalks; identifying, classifying, and interacting with objects and environments; and engaging with computers and digital devices. Human vision continues to develop and be fine-tuned by technology to support an ever-increasing range of dynamic events and human experiences. Yet, as our society continues to invest in R&D to advance and deploy new technology and automation techniques, there are increasing opportunities for businesses and consumers to leverage or pair (i.e., in a cooperative or human-in-the-loop manner) human sight with computer-driven sight (referred to as computer vision [CV] or computer vision artificial intelligence [CV AI]) to take the next step in delivering improved productivity, efficiency, safety, sustainability, and inclusivity.

CV has been a strong beneficiary of academic and commercialization investments to advance the fields of deep learning– and machine learning (ML)–based approaches to AI. These advancements, which have largely occurred over the past five years, look to abstract the human intelligence schema and system to interpret unstructured data in the forms of images, videos, and sensor data (e.g., radar, lidar) through complex neural networks. To develop this neural network architecture, CV technology user organizations require massive amounts of use case–specific or even generalizable training data, as well as extensive computational resources (including GPUs, TPUs, and hardware- and software- based accelerators) to train, build, and validate models that can “learn” details and characteristics from new, unstructured visual-based inputs. This approach to solving CV AI has led to breakthroughs where computers are now able to surpass the quality and efficiency of humans for multiple discrete use cases, along with delivering differentiated benefits versus humans in the areas of scale, repeatability, longevity, attentiveness, and subjectivity (to name a few).

Although deep learning–based CV is a very new technology area, IDC has seen tremendous progress in its use by organizations of all sizes and across all verticals. This includes support for (or even potentially enabling new) business and consumer use cases that can deliver insights in the areas of:

- Anomaly detection

- Augmented reality/virtual reality (AR/VR) applications ▪ Assembly line automation

- Asset predictive maintenance

- Digital twins

- Facial recognition and detection

- Fraud detection

- Geospatial analysis and analytics

- Health and safety compliance

- Identity and access management

- Intelligent document processing (IDP)

- Inventory management

- Media analysis and compliance

- Medical imaging

- On- or off-road autonomous/automated driving

- Optical character recognition (OCR)

- Process and task automation

- Roadway compliance, optimization, or tolling (e.g., registration, speed, parking) ▪ Security and facility management

- Sentiment analysis

- Shopper analytics

- Visual inspection and quality control

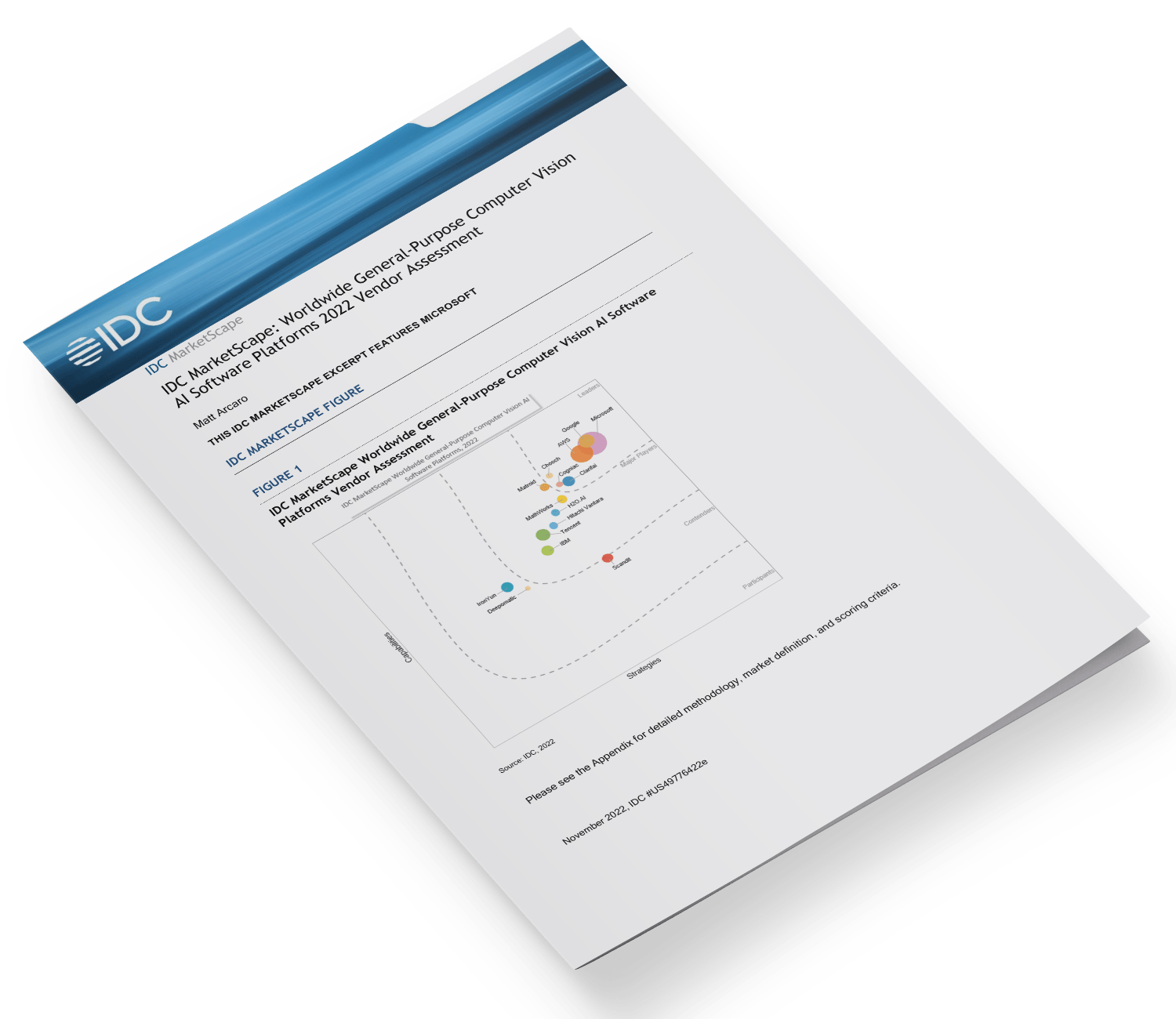

This IDC MarketScape focuses on one aspect of the CV ecosystem, CV software platform providers. These essential vendors make up the foundation of growth and potential of CV, and they enable customers to understand, experiment, develop, train, validate, deploy, and manage CV models for a near-infinite list of potential use cases. These providers are critical to helping customers extract the complexity of working with, utilizing, and managing CV deployments, as well as helping them understand how cutting-edge AI research techniques and approaches equate ultimately to business value. In many cases, these providers offer different low-code and no-code user interface/user experience (UI/UX) options to support organizations with a mix of potential user personas ranging from AI/ML technical specialists (e.g., data scientists, ML engineers) to traditional IT personnel (e.g., developers and computer programmers) and even line-of-business users (e.g., payroll and accounting staff).

As part of this IDC MarketScape process, IDC spoke with dozens of end-user organizations that are investing in CV platform providers to help them develop and deploy applications. These organizations, which all varied in terms of CV deployment maturity, were almost universally aligned on the tangible, business benefits provided by these CV solutions, as well as (more importantly) recognized that they should have prioritized and invested in CV earlier. These conversations reinforce the need for organizations (broadly) to think through how CV can be used to improve business, consumer, and partner interactions and capabilities both at a strategic, governance level and at a specific use case level.